V

主页

京东 11.11 红包

08 Multiple-Period Risk-Neutral Valuation

发布人

学习爱我!数学爱我!考试爱我! 宅家学习一波啊~科科(●ˇ∀ˇ●)

打开封面

下载高清视频

观看高清视频

视频下载器

IFM_1Introductory Derivatives - Forwards and Futures

4 Coherent Risk Measures

10 Multiple-Period Binomial Option Pricing - Example

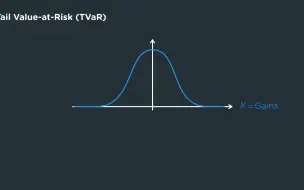

3 Tail Value-at-Risk (TVaR)

IFM_7MeanVariance Portfolio Theory

09 Multiple-Period Replicating Portfolio Approach

2 Empirical Evidence Supporting the EMH

IFM——6GeneralPropertiesofOptionsPart2

10 Diversification with an Equally-Weighted Portfolio

07 Multiple-Period Binomial Option Pricing

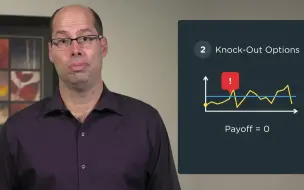

01 Barrier Options

08Put Options - Payoffs

10 Fitting Stock Prices to a Lognormal Distribution

16 Combining Risky Assets with Risk-Free Assets

09 Portfolio Elasticity and Risk Premium

11 Levered Firms as Comparables - continued

09 Risk-Neutral Pricing

19 Guarantee Value Formulas, Underlying

8 The Volatility of a Large Portfolio

19 Combining Options - Ratio Spread

3 Empirical Evidence Against the EMH- Market Anomalies

24 Combining Options - Strangle

14 Combining Options - Bull Spread Example

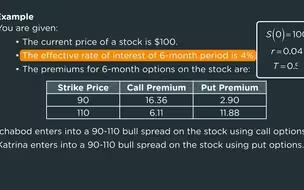

13 Combining Options - Bull Spread

01 Bounds of Option Prices - Lower Bounds

11 Diversification with a General Portfolio

02Options as Insurance

02 Lognormal Model for Stock Prices - Distribution

22 Options - Collared Stock

16 MM Proposition II (Without Taxes) - WACC with Multiple Securities

08 Strike Price Effects

5 The Behavior of Individual Investors

3 Pre-Money and Post-Money Valuation

02 Asian Options - Example 1

44Synthetic Positions - Synthetic Treasury

1 Forms of Market Efficiency

9 Corporate Debt

20 Factors Affecting the Timing of Investments

4 The Efficiency of the Market Portfolio

IFM_10 Investment Risk and Project Analysis