V

主页

京东 11.11 红包

4. Percentiles, Mode, Skewness, _ Kurtosis

发布人

学习爱我!数学爱我!考试爱我! 宅家学习一波啊~科科(●ˇ∀ˇ●)

打开封面

下载高清视频

观看高清视频

视频下载器

IFM——9Market Efficiency and Behavioral Finance

2. Geometric

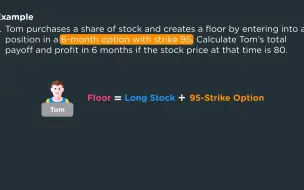

IFM——2General Propertiesof OptionsPart 1——4comparing option

13 Efficient Portfolios

2. Hypergeometric

01 The Normal Distribution vs. The Lognormal Distribution

03 Greeks - Vega, Rho, and Psi

6 Mechanics of an IPO

IFM——6GeneralPropertiesofOptionsPart2

11 Delta-Hedging

3. Discrete Uniform

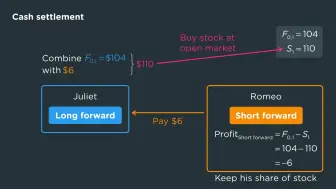

IFM_1Introductory Derivatives - Forwards and Futures

2 Value-at-Risk (VaR)

06 Options as Insurance - Example

2025卫生统计学 19课时

22 Use of Derivatives to Manage Risk in Insurance and Annuity Products

3 The Capital Asset Pricing Model (CAPM)

5 Initial Public Offering

03 Option Pricing- Replicating Portfolio - Example

05 Lognormal Model for Stock Prices - Percentiles

03 Relationship between Gap and Ordinary Options

2. Bernoulli

05 Call Options - Profits

24 Combining Options - Strangle

17 Optimal Investor Portfolio

13 MM Proposition I (Without Taxes) - Examples

03 Asian Options - Example 2

16 Introduction

3. Continuous Uniform

04 Call Options - Payoffs

10 The Delta-Gamma-Theta Approximation

10 Diversification with an Equally-Weighted Portfolio

07 Conditional Stock Prices

2. Shifting and Scaling

17 Guarantees in Variable17 Annuity Products

10Graphing Payoffs - Shortcut Method for Calls and Puts

2. Univariate CDF Method

2 Equity Funding for Private Companies

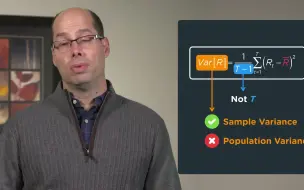

3 Historical Variance and Volatility