V

主页

2.1.7 相关性的基础知识:定义、应用和术语

发布人

点击链接查看更多内容:https://analystprep.com/shop/frm-part-1-and-part-2-complete-course-by-analystprep/ AnalystPrep是经GARP批准的FRM学习平台。内容包括所有关于FRM的视频课程、学习笔记、题库、模拟考试和涵盖FRM大纲所有章节的公式表。 Correlation Basics: Definitions, Applications, and Terminology

打开封面

下载高清视频

观看高清视频

视频下载器

2.1.15 波动率微笑 Volatility Smiles

2.5.2 因素 Factors

1.4.2 计算与应用 VaR Calculating and Applying VaR

2.1.5 VaR 映射 VaR Mapping

2.1.8 相关性的经验属性:相关性在现实世界中是如何表现的?

2.5.1 因素理论 Factor Theory

【泳者之心】游过偏见之海,书写女性传奇!

1.3.1 银行 Banks

1.3.16 利率的性质 Properties of Interest Rates

1.3.20 互换 Swaps

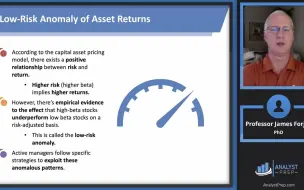

2.5.3 阿尔法(和低风险的异常现象)Alpha (and the Low-Risk Anomaly)

2.1.14 期限结构模型的艺术:波动性和分布

2.5.4 投资组合构建 Portfolio Construction

1.4.13 非平行期限结构转变的建模和对冲 Modeling and Hedging Non-Parallel Term Structure Shifts

1.1.5 MPT 与 CAPM MPT and CAPM

2.2.5 信用风险和信用衍生工具 Credit Risks and Credit Derivatives

2.1.11 期限结构模型的科学 The Science of Term Structure Models

1.3.3 基金管理 Fund Management

1.1.7 风险数据汇总和报告原则 Risk Data Aggregation and Reporting Principles

2.4.1 流动性风险 Liquidity Risk

2.1.12 短期利率的演变和期限结构的形状

2.3.5 风险缓解 Risk Mitigation

1.5.6 时间轴—你最好的朋友 Timelines – Your Best Friends

1.4.12 应用久期、凸性与DV01 Applying Duration, Convexity, and DV01

2.1.6 学术文献中关于交易账簿风险计量的信息

2.5.9 对冲基金 Hedge Funds

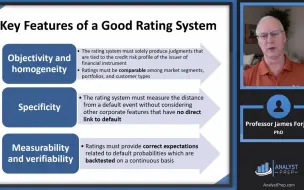

2.2.4 评级方法 Ratings Assignment Methodologies

1.3.17 公司债券 Corporate Bonds

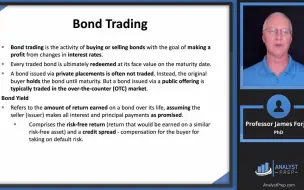

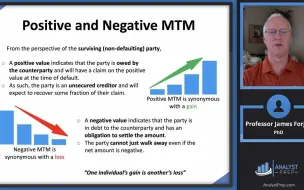

2.2.12 信贷风险和融资 Credit Exposure and Funding

2.3.3 风险识别 Risk Identification

2.2.2 信贷分析 The Credit Analyst

1.3.12 期权市场 Options Markets

1.4.3 衡量和监测波动率 Measuring and Monitoring Volatility

1.5.12 零假设和非零假设 Null and Alternative Hypotheses

2.1.13 期限结构模型的艺术:漂移 The Art of Term Structure Models: Drift

1.2.10 平稳时间序列 Stationary Time Series

1.4.6 信用风险测度 Measuring Credit Risk

2.2.16 信用风险转移市场及其影响 The Credit Transfer Markets and Their Implications

2.2.17&18 证券化简介 An Introduction to Securitization

1.3.15 奇异期权 Exotic Options